Can I Foster if I Have Debt or a CCJ? Understanding the Eligibility Criteria

Fostering is a noble commitment that can change a child’s life, but many potential foster carers worry about their financial situations, particularly if they have debt or a County Court Judgment (CCJ). Understanding how these financial issues affect your eligibility to foster is crucial. Let’s delve into this important topic to help clarify your concerns.

Firstly, it’s vital to recognize that local authorities assess various factors when determining whether someone is suitable to become a foster carer. Money issues, including personal debt or a CCJ, may come into play, but they are not automatically disqualifying factors. Instead, your financial situation will be reviewed in the context of your overall ability to provide a stable and nurturing environment for a child.

Factors that influence your eligibility include:

- Your financial stability and ability to manage your budget

- Your circumstances surrounding the debt or CCJ

- Your commitment to fostering and willingness to support children in need

If you have debt, it’s essential to show that you are managing it responsibly. Foster care agencies want to ensure that you can provide for a child’s needs without your financial situation causing additional stress. If you can demonstrate a steady income and a plan to address your debts, this might positively influence the agency’s decision.

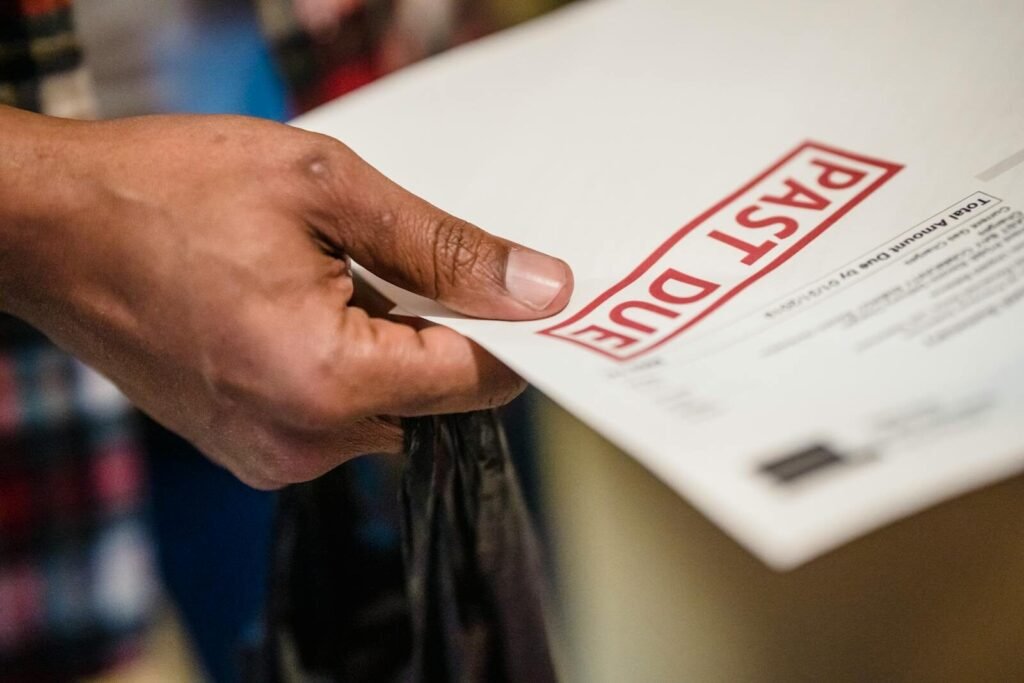

Having a CCJ can raise concerns among fostering agencies, but it does not automatically disqualify you. Typically, the local authority will consider factors such as:

- The reason for the CCJ

- How long ago it was incurred

- Your current financial stability and progress towards resolving the issues

For those with a CCJ, it’s crucial to show that you’ve learned from past mistakes and are now in a responsible financial position. Providing proof of regular payments towards the judgment can demonstrate your commitment to rectifying the situation.

When applying to become a foster carer, be prepared to discuss your financial history openly. Honesty is essential, as any discrepancies might hinder your application. Social workers conducting assessments want to understand your whole life situation, and this transparency will help build trust.

Moreover, it’s worth noting that fostering agencies are often more focused on your emotional stability, resilience, and the environment you can provide for a child, rather than just your financial status. Many successful foster parents have faced similar challenges and have emerged stronger and more capable.

Consider the following tips if you’re concerned about your financial situation:

- Create a Budget: A budget will help you track your expenses and income. This can also show the fostering agency that you’re financially responsible.

- Seek Financial Advice: Talking to a financial advisor can help you manage your debt more effectively and develop a plan to handle your finances.

- Be Transparent: When fostering agencies ask about your financial history, be open about your situation. This builds trust and may help mitigate concerns.

It’s essential to remember that every case is treated individually. Your location, the fostering agency, and specific circumstances surrounding your financial history will all play a role in the decision. It’s best to contact local fostering agencies directly to get tailored advice and understand their specific requirements regarding debt and CCJs.

If you are passionate about fostering and genuinely want to help a child, take the time to address your financial situation. With the right approach, compassion, and clarity about your circumstances, you can navigate the fostering process and provide a safe and loving home for a child in need.

Having debt or a CCJ does not disqualify you from fostering. Instead, focus on showcasing your merit as a responsible and caring individual who can provide a supportive environment for children. Your commitment and desire to foster can shine through, even in the face of financial challenges.

Financial Stability and Its Role in Foster Care Applications

When considering the journey of fostering a child, many prospective foster carers often wonder about their financial situation. Questions arise like, “Can I foster if I have debt or a CCJ?” Understanding how your financial stability impacts your foster care application is essential. Financial circumstances can play a significant role in the assessment of your suitability as a foster parent.

To begin with, fostering agencies look at your overall financial health to evaluate your ability to provide for a child. While it is understandably concerning to think about how debt could affect your application, having debt or a CCJ (County Court Judgment) does not automatically disqualify you from fostering. It’s crucial to understand how these factors are evaluated and what steps you can take to improve your chances.

The Importance of Financial Stability

Financial stability is more about your ability to manage your finances rather than having a perfect credit score. Foster agencies assess whether you can provide a safe and nurturing environment for a child. Here are some aspects they consider:

- Budgeting Skills: Agencies look for applicants who can manage their finances responsibly. Demonstrating that you can create and stick to a budget shows that you can handle the additional expenses of fostering.

- Income Sources: Your employment status and income sources matter. Steady income can provide reassurance that you can support a child’s needs, including food, clothes, and extracurricular activities.

- Handling Debt: It’s essential to show how you manage your existing debt. If you’re actively working to pay it down and can prove that it’s under control, this will reflect positively on your application.

- Support Systems: Having a support network, whether through family, friends, or community resources, can help bolster your financial stability. This network could offer assistance if unforeseen expenses arise.

How Debt and CCJs Are Assessed

When reviewing your application, agencies will assess how your financial situation impacts your ability to foster. Debt, including credit card debt, loans, or other obligations, will factor into their decision. Here are key points they will scrutinize:

- Type of Debt: Secured debts (like mortgages) may be viewed more favorably than unsecured debts (like credit cards). If you have a clear plan for managing your unsecured debts, this can help.

- CCJ Impact: While a CCJ can be a red flag, it doesn’t mean the end of your fostering journey. If you have addressed the CCJ and are on a repayment plan, be open about it during your assessment.

- Transparency: Being honest about your financial situation will go a long way. Agencies appreciate transparency and a willingness to discuss how you manage financial challenges.

Steps to Take if You Have Debt or a CCJ

If you are serious about fostering but are concerned about your financial situation, there are proactive steps you can take:

- Consult Financial Advisors: Professional advice can help you create a clear plan for managing your debt effectively.

- Create a Payment Plan: If you have debt, work on forming a structured repayment plan to show that you are actively managing your finances.

- Rebuild Your Credit: Start taking steps to rebuild your credit score. This may include making timely payments on bills and paying down debts.

- Educate Yourself: Attend workshops or counseling programs focused on finance management. This will show fostering agencies your commitment to improving your situation.

Ultimately, while your financial health is an important factor, it isn’t the sole determinant in fostering assessments. Respecting the process and focusing on becoming financially stable can positively influence your application. With the right approach and commitment to handling your finances well, it’s still very possible to go ahead with fostering, even if debt or a CCJ is part of your story.

Remember, fostering is about providing a loving home for a child who needs it. Your ability to nurture and care for them will always matter more than your financial situation, as long as you are proactive and responsible in managing your circumstances.

The Impact of Debt on Parenting and Nurturing Abilities

Being in debt or facing a County Court Judgment (CCJ) can be difficult and stressful. When you are a parent or caregiver, financial stress can also affect your ability to nurture and provide for your children. Understanding the impact of debt on parenting is vital for anyone considering fostering or raising children in such circumstances.

Financial troubles can often lead to emotional strain. This stress can affect how you interact with your child. Children thrive in stable environments where they feel safe and secure. If you’re worried about money, it can be hard to focus on their needs. Children can sense when their parents are anxious or upset, and this can lead to feelings of insecurity and worry in them.

Debt can shift your priorities. When struggling financially, you may focus more on making ends meet rather than nurturing your child’s emotional and physical needs. This imbalance can leave children feeling neglected. It’s essential to create a supportive environment where children can flourish, regardless of your financial situation. You can do this by finding ways to stay engaged with them, even if times are tough.

Many parents worry that having debt will affect their ability to qualify for fostering. It’s essential to know that each fostering agency has different requirements. Some agencies may overlook financial struggles if you can demonstrate stability in other areas of your life. However, consistent communication about your financial situation and how you manage it can be crucial.

The Effects of Debt on Parenting

Understanding how debt impacts your parenting style is important. Here are some ways financial stress can influence your ability to nurture:

- Emotional Well-Being: Ongoing stress from debt may lead to mental health struggles, such as anxiety or depression. These challenges can make patience and positivity more difficult, which are essential aspects of parenting.

- Time Management: If you’re working multiple jobs to pay off debts, you may have less time to spend with your children. Quality time is vital for building strong parent-child relationships.

- Resource Allocation: Financial strain may limit your ability to provide essential resources, like a good education or extracurricular activities, which can hinder your child’s development.

- Role Modeling: Children learn important lessons from watching their parents. If they see you struggling with debt, they might develop a distorted understanding of financial responsibility.

- Impact on Communication: Financial stress can create tension in conversations. This tension can prevent open dialogues about feelings, which are essential for developing emotional intelligence.

Finding Balance

While debt can create challenges, there are ways to nurture effectively even in difficult financial situations:

- Open Conversations: Being transparent with your children about financial matters, suitable for their age, can help them understand the situation. This can provide them with tools to manage their anxieties around money.

- Quality Time: Focus on low-cost activities like playing games, going for walks, or reading together. These actions show your commitment and love, regardless of financial status.

- Seek Support: Counseling and support groups can offer emotional relief. Connecting with other parents can provide new strategies for coping with both parenting and financial difficulties.

- Set Goals: Involve your children in setting small financial goals. This teaches valuable lessons about responsibility and collaboration.

- Prioritize Self-Care: Make space for your own well-being. Taking care of yourself ensures you’re in a better position to nurture your children.

Ultimately, while debt can present obstacles, it doesn’t have to define your ability to parent effectively. By addressing both emotional and financial aspects, you can create a loving and nurturing environment for your children.

If you are considering fostering while facing financial difficulties, it’s important to keep an open dialogue with agency workers. They can guide you and identify the support you may need to ensure a successful fostering experience.

Fostering can be a rewarding experience that brings joy and fulfillment. Don’t let financial challenges deter you from considering this path. With courage and communication, you can navigate the path ahead.

Support Systems for Foster Parents with Financial Challenges

Fostering can be a rewarding journey, providing a loving home for children in need. However, financial challenges can pose significant hurdles for prospective foster parents. Understanding the support systems available to navigate these challenges is essential for anyone considering this path.

Many agencies and organizations recognize the importance of supporting foster parents, particularly those facing financial difficulties. One of the most significant resources available is financial assistance for foster care. This often includes monthly stipends for the care of each child placed in a foster home. The amount can vary based on factors such as the child’s age and specific needs. It’s important for foster parents to check with their local state or county agencies to understand the specifics of these financial supports.

In addition to monthly stipends, there are often additional funds available for special needs. If a child has medical or psychological conditions that require extra care, foster parents may be eligible for additional financial assistance. This can include funds for therapy, medications, or specialized care, easing the burden on foster families.

Another valuable resource for foster parents coping with financial challenges is community support programs. Local nonprofits, religious organizations, and community groups often provide assistance in various forms, including:

- Food Pantries: Many communities offer food banks or pantries that provide free groceries, significantly reducing monthly living expenses.

- Clothing Drives: Foster children need clothing, and there are numerous charitable organizations that collect and distribute clothes for free or at a minimal cost.

- Emergency Funds: Some organizations set aside emergency funds to help foster families address urgent needs, such as unexpected medical bills.

- Transportation Services: For parents who strain under the cost of transporting children to appointments or school, some community programs offer free or subsidized transport services.

Foster parents should also look into workshops and training programs that not only enhance their parenting skills but may also provide financial education. Many foster care agencies offer training that focuses on budgeting and financial planning. These resources can empower parents to manage their finances more effectively and become more adept at dealing with the costs associated with parenting.

State-sponsored programs are another lifeline for foster families. For instance, many states have initiatives that provide supplementary financial support to parents struggling to maintain a stable home environment for foster children. It’s crucial for potential foster parents to reach out to state child welfare services to inquire about these programs. They can also provide guidance on navigating the complexities of debt and financial instability while fostering.

Moreover, foster parents can connect with support groups where they can share experiences, gain insights, and access resources. These groups often work together to address financial hardships, pooling their knowledge to find creative solutions. Online forums and social media groups specifically for foster parents offer vast networks of support that can help families feel less isolated in facing their challenges.

It’s also wise for foster parents to educate themselves about their rights regarding financial aid. Understanding state and federal laws about assistance for foster families can reveal opportunities for aid that are not always immediately apparent. For example, some states offer tax credits for foster parents, which can offset some expenses and reduce the overall financial burden of fostering.

If a foster parent struggles with debt or has a CCJ (County Court Judgment), being open and honest with the fostering agency is crucial. Transparency about financial status can lead to targeted support and resources that may not otherwise be available. Agencies want to ensure that all families can provide a safe and loving environment for children, which sometimes includes addressing financial issues through direct assistance or counseling.

Building a strong personal support network can make a significant difference. Friends, family, and neighbors can often assist foster parents with childcare, transportation, or other forms of support, which can relieve some financial pressures. By working together with community organizations, fostering agencies, and their personal connections, families can create a robust support system that helps alleviate the strain of financial challenges.

Ultimately, while financial issues can seem daunting, there are numerous resources designed to support foster parents. Exploring these can lead to a more manageable experience, allowing focus on the important work of providing a loving and stable home for children in care.

Steps to Improve Financial Health Before Fostering

Fostering children is a rewarding but significant responsibility. As you consider opening your home to a child in need, ensuring your financial health is crucial. Managing debts or dealing with a CCJ can feel overwhelming, but taking proactive steps can prepare you for fostering. Here are some methods you can adopt to improve your financial situation.

Assess Your Financial Situation

The first step to improving your financial health is understanding where you stand. Create a detailed budget that outlines your income, expenses, debts, and savings. Use this information to gain a clearer picture of your financial landscape.

Track Your Income and Expenses

Document all sources of income, including salaries, benefits, and any side jobs. Next, list all monthly expenses. Be sure to categorize them into fixed (like rent) and variable expenses (like groceries). This will help you spot areas where you can cut back and save money.

Develop a Debt Repayment Plan

If you have debts or a CCJ, creating a solid repayment plan is essential. Focus on paying off high-interest debts first, as they cost you the most over time.

Prioritize Your Debts

Consider using the debt avalanche or snowball method. The avalanche method suggests targeting debts with the highest interest rates first while maintaining minimum payments on others. The snowball method, on the other hand, involves paying off the smallest debts first to build momentum. Choose the strategy that feels right for you.

Seek Financial Advice

If your financial situation feels unmanageable, reaching out for professional help can be beneficial. There are various resources available, from credit counseling agencies to personal finance advisors who can guide you through your challenges. They can help you understand your options and create a realistic plan for improvement.

Build an Emergency Fund

An emergency fund can provide peace of mind and financial stability. Aim to save at least three to six months’ worth of living expenses to weather unexpected costs that may arise. Start small with manageable savings goals, gradually increasing your contributions as you find more financial flexibility.

Automate Savings

Consider setting up an automatic transfer from your checking account to your savings account each payday. This makes saving easier and lessens the temptation to spend the money instead.

Improve Your Credit Health

Your credit score plays a significant role in your financial life, especially when it comes to fostering arrangements that might require financial assessments. Improving your credit takes time, but specific actions can help elevate your score.

Pay Your Bills on Time

One of the most effective ways to boost your credit score is to ensure that all bills are paid accurately and on time. Set reminders or automate payments to avoid late fees and negative credit reporting.

Limit New Credit Applications

While you might be tempted to apply for new credit cards or loans, too many inquiries can negatively impact your credit score. Focus on stabilizing your existing credit accounts first before seeking new lines of credit.

Consider Additional Income Streams

The prospect of fostering can add financial pressure, especially if you are already managing debts. Exploring ways to increase your income can help alleviate some of this stress.

Explore Side Gigs or Freelancing

- Look for part-time jobs that fit your existing schedule.

- Consider freelancing in any skills you possess, such as writing, graphic design, or tutoring.

- Explore online platforms that offer payment for completing various tasks, like surveys or website testing.

Review and Adjust Regularly

Your financial situation is not static, so regularly reviewing your budget and adjusting it as needed is essential. Life changes, unexpected expenses, and income fluctuations should all prompt a reevaluation of your financial health.

Taking these steps can help you improve your financial health, making you more prepared when considering fostering a child. Remember, investing time in your financial well-being today ensures a brighter and more stable future for you and the children who may enter your home.

Conclusion

Fostering is a noble responsibility that can bring profound joy and fulfillment, but it also requires careful consideration of various factors, including financial health. While having debt or a CCJ may raise concerns about your eligibility to foster, it’s important to understand that every situation is unique. Many fostering agencies recognize that financial stability is essential, but they also look at the overall capability of an individual to provide a loving and nurturing environment for a child.

Your past financial challenges don’t define your potential as a foster parent. The key lies in demonstrating your commitment to overcoming these obstacles, which can showcase your resilience and determination. Understanding how debt might affect your parenting skills is crucial; being financially secure allows you to focus more on the emotional and physical needs of a child, setting a strong foundation for their growth and well-being.

Fortunately, there are support systems in place for those who face financial difficulties while pursuing fostering. Many organizations offer resources, advice, and assistance to help you navigate your financial situation. Seeking these supports can ease the burden and prepare you better for fostering.

Additionally, taking proactive steps to enhance your financial health not only helps your application but also empowers you as a potential foster parent. This journey can involve budgeting, debt management, or seeking professional financial advice. By working on your financial literacy and stability, you can create a safe and nurturing space for a child in need, proving that love and care can thrive, even when challenges arise.